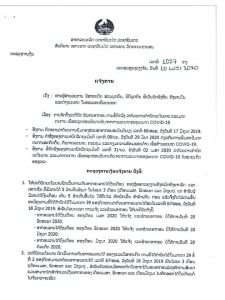

The Ministry of Finance issued the Notification No.1027, dated on 10 April 2020, further the Prime Minister’s Decision No.31, on measures to mitigate the impact of the COVID-19 outbreak. This Notification announces tax exemptions on personal income.

Please find below the main points of the Notification, summarized by our member DFDL:

- Salaries of LAK 5 million or below for all employees (whether public or private) will be exempt from personal income tax (“PIT”) for three months (April, May and June). For employees with salary levels above LAK 5 million, the first LAK 5 million will be exempt from the PIT calculation. Salary income above this LAK 5 million threshold will be taxed at progressive rates of 10%-25% in accordance with Article 39 of the Income Tax Law. The PIT filing and tax payment deadlines remain the 20th of the following month.

- An income tax exemption for micro-enterprises (as described in the Income Tax Law) for three months (April, May and June 2020). Micro-enterprises that have already made prepayments of income tax for April, May and June under a contract with the tax authorities can carry such payments forward to be used as a deduction in the following months.

- Those who pay PIT under the lump sum tax system in accordance with a concession agreement must continue to declare and pay such PIT and will not be eligible to the exemptions described in Item 1 above.

- Taxpayers can declare and pay PIT through the normal process. The TaxRIS online filing system will automatically exempt the first LAK 5 million of salary when calculating PIT.

Please find the Lao version below (the English translation will be uploaded on a later date)